Gartner Magic Quadrant „Content Services Platforms“ (CSP) Q4 2019

30. Oktober 2019 13:22 Uhr | | Permalink

Der “ Gartner Magic Quadrant for Content Services Platforms“, verfasst von den Analysten Marko Sillanpaa, Michael Woodbridge und Lane Severson, wurde am 30.10.2019 veröffentlicht. Er kann bei verschiedenen Anbietern (z.B. Hyland) nach der Freigabe im November heruntergeladen werden.

Gartner beschränkt den Quadranten auf CSP Content Services Platforms (also traditionelle ECM Lösungen) und lässt CSA Content Services Applications (wie eAkte- oder Rechnungseingangsanwendungen) und CSC Content Services Components (wie OCR- oder PDF-Konverter-Dienste) außen vor. Content Services Platforms sieht Gartner als Schlüsselkomponenten für den Digital Workplace und Digital Business an – um zwei weitere, unspezifizierte Schlagworte einzuführen. Schwerpunkte der Bewertung liegen auf Cloud-Lösungen, Benutzerfreundlichkeit (ease of use), Künstliche Intelligenz (KI/AI) und Information Governance. Zielgruppe sind große Anwenderorganisationen auf der Suche nach geeigneten „Digital-Workplace“-Lösungen. Der Fokus verschiebt sich damit im Vergleich zu den Vorjahren nochmals. Interessant ist dabei, dass die eigentlich wichtigen Lösungen – nämlich die Content Services Anwendungen – , mit denen die Anwender arbeiten sollen, außen vor bleiben. Nicht gerade hilfreich für Entscheidungen.

Gartner definiert den Markt für Content Services in den PeerInsights kurz wie folgt:

„Content services platforms (CSPs) are integrated platforms that provide content-focused services, repositories, APIs, solutions and business processing tools to support digital business and transformation. Typical CSP use cases include document management, back-office processes, business process applications, records management and team productivity. A CSP has its own repository. CSP services and data may also integrate with external, non-native repositories and applications through prebuilt connectors, API development or prepackaged integrations. CSPs have web, desktop and mobile app interfaces that let users navigate through and work with the different content services. The platforms may also offer prebuilt solutions for vertical and horizontal content processes such as case management, legal matter management, contract management. CSPs are available on-premises, as hosted services, in the cloud (SaaS and/or PaaS) or in hybrid architectures that combine cloud and on-premises storage and/or services.“

Im Magic Quadrant wird das Thema CSP Content Services Platforms wie folgt erläutert:

„Market Definition/Description (revised version Oct. 30th, 2019)

The content services platform (CSP) market contains both long-established vendors and relatively new vendors. Both kinds sell products to support the content- and process-related needs of operational business functions. They support a broad range of these functions, ranging from horizontal ones such as HR employee onboarding to industry-specific ones such as insurance claims management. To support this breadth, they need to combine capabilities including robust content and metadata management, process automation, intelligent classification and information governance. Integration with common business applications via configuration is also key.

Buyers’ needs for CSP technologies have shifted over the past few years. There is increased focus on three trends that are present across organizations, regardless of industry:

- Tackling content sprawl:

Organizations have a multitude of content repositories, and with the increasing prevalence of SaaS, more silos materialize on a regular basis. The desire to rationalize this multitude of content sources did not disappear with the death of enterprise content management (ECM). Fortunately, there is an acceptance in the market that new techniques are required to tackle this issue. - Delivering digital business transformation:

CSP technology is in demand to underpin new operations and processes that utilize content as a key component in innovative ways. A common requirement is to join up fragmented operations by including partners, suppliers and customers directly in system processes that include both operational and collaborative experiences. An insurance company might digitize and join up the entire claims processing cycle, for example. Customers can then interact directly with the organization’s back office, which, in turn, can collaborate effectively with other partners in the process. The open, yet secure combination of content and processes is an enabler of this kind of transformation. - Modernizing work:

Users’ expectations have changed for good, due to the ubiquity of compelling user experiences in consumer applications. There is increasing evidence that a workforce with a high degree of digital dexterity is more likely to help an organization realize its digital transformational goals. New modes of interaction with content (for example, synchronous editing in a non document format such as Dropbox Paper) are required in order to modernize the work experience.

Buyers’ needs require more agile, adaptive solutions, which are very different to the rigid, on-premises and monolithic solutions of old. At the heart of any digital business platform, a modern CSP must display the following characteristics:

- Cloud scale:

The ability to scale to meet the demands of the workforce. Provision o seamless connectivity to a broad ecosystem of suppliers, partners and customers, while delivering continuous innovation, is essential. - Protection:

The provision of deeply embedded, flexible and intelligent information governance, security and privacy controls. This is essential to operate in a world of ever increasing threats and regulatory demands. - Fast time to value:

The ability to deliver business value quickly — for example, through the provision of pre-built applications and citizen-developer-based tools. - User-centricity:

A consumerized user experience with embedded mobility and consistency across devices. A focus on the overall user experience is of paramount importance for driving adoption and realizing the expected benefits of this technology. - Intelligence:

Advances in artificial intelligence (AI) techniques, including machine learning (ML) and deep neural networks, have enabled innovations for classification, productivity and automation scenarios. Such capabilities should be embedded in all key areas of the platform, from security to collaboration, to align with the evolving expectations of the market.

Gartner’s assessment of the CSP market focuses on the ability to provide solutions for the underlying business needs outlined above. There are several ways in which functionality and features can be implemented to support the characteristics listed above.“

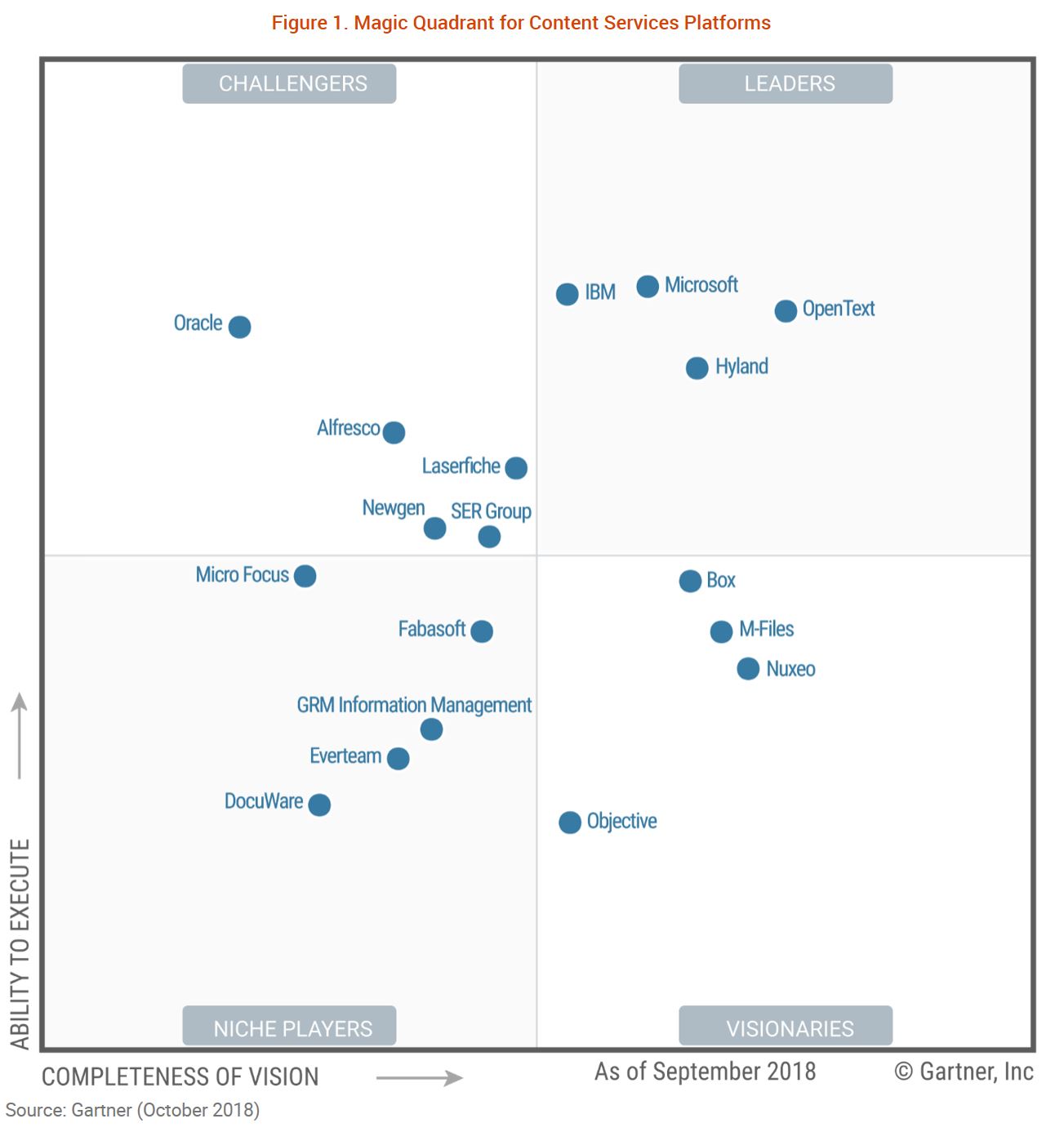

Magic Quadrant for Content Services Platforms (CSP) Oct. 2019

Bewertet wurden die Unternehmen Alfresco, AODocs, Box, DocuWare, Everteam, Hyland, IBM, iManage, Laserfiche, M-Files, Micro Focus, Microsoft, NetDocuments, Newgen, Nuxeo, Objective, OpenText und SER. Einige wie Fabasoft, GRM und Oracle sind heraus gefallen, andere wie AODocs, iManage (erneut dabei) und NetDocuments sind hinzugekommen. Wie immer wichtig: nicht den Quadranten interpretieren sondern die einzelnen Einschätzungen und Bewertungen im Text konsultieren. Gartner schreibt hierzu deutlich:

„This Magic Quadrant represents a snapshot of the CSP market (as we define it). It will help you select a CSP vendor, but do not use it as your only aid. You should also consult the companion “Critical Capabilities for Content Services Platforms” [2018], which will prove especially helpful for identifying vendors for particular use cases. Your final selection criteria must reflect your organization’s functional and technical requirements and business objectives. Do not, for example, select Leader or reject a Niche Player simply on the basis on those labels. Assess any vendor that meets your “must have” requirements — a vendor in any one of the four quadrants could be the best choice for your needs.“

Im Leaders-Quadrant finden sich nicht nur die gleichen „Verdächtigen“ wie 2018: Microsoft, OpenText, Hyland und IBM. Box rückt aus dem Visionaries Quadrant auf und findet sich jetzt ebenfalls im Leaders Quadrant.

Dicht beieinander im Challengers Quadrant sind Alfresco, SER, Laserfiche und Newgen angesiedelt. Oracle ist hier jetzt endlich raus.

Bei den Visionaries rücken zwei Anbieter langsam in Richtung Leaders: M-Files und Nuxeo.

Im Niche Players (und Nachrücker) Quadrant finden sich bunt aufgereiht Objective, Everteam, iManage, NetDocuments, Docuware und Micro Focus. Etwas abgesetzt der Newcomer AODocs.

Unter den erwähnenswerten „Honorable Mentions“ ist diesmal auch Easy Software aus Deutschland. Dazukommen EISOO mit Schwerpunkt in China und anderen asiatischen Staaten und ASG (die ihre Vertriebsaktivitäten mit Mobius gerade in Deutschland intensivieren),

„Context

Having evolved from the long-standing ECM market, the CSP market is relatively mature. Differentiation purely in terms of features and functions can therefore be hard for vendors to achieve. However, this market is modernizing. Content plays such an important role in digital transformation initiatives that clients require agile, adaptive platforms. Gartner’s interactions with clients looking to purchase CSPs indicate specific demands for:

- A highly integrated and consumerized user experience with consistency across all devices

- The ability to derive value from investments in CSPs more quickly

- Cloud modes of delivery, with innovations being delivered quickly and frequently, even where hybrid deployment models are used

- Intelligence and automation embedded into all functions, from productivity capabilities to security controls

- Transparent and robust information governance and security, along with tools to manage these areas cost-effectively

Vendors have responded to these demands by adding new services and capabilities to their products. Their communication of these additions can be confusing, however, as common terms are used to mean different things, “AI” and “cloud” being notable examples. Customers should be aware of the developing capabilities of vendors in the following areas, and should check how these are implemented to ensure suitability for their technology strategy:

- User experience:

Over the past few years, most vendors have considerably updated the user experiences they provide, with many now delivering compelling, modern experiences across a range of devices. But it is important to evaluate how far these developments spread through their entire product stack. Vendors with large application portfolios have not deployed user experience improvements consistently across all their products, so the user experience can sometimes be inconsistent. - Time to value:

A major factor in any CSP purchasing decision must be how quickly the customer can derive business value from a solution. Vendors can shorten the “time to value” in a variety of ways. The quickest is to provide prebuilt applications, thus enabling immediate deployment and usage for given business scenarios. Low-code/no-code configuration tools provide further options for extending these applications or building entirely custom solutions without having to revert to more complex development methods. Beyond these approaches, the API layer is important, as is the ability of the customer’s in-house IT unit to utilize this effectively alongside the existing application ecosystem. Vendors’ offerings range from those that provide native APIs, to those that offer microservices-based REST APIs, and those that supply well-rounded developer SDKs. - Cloud delivery models:

Most CSP vendors now provide and promote SaaS platforms, with continuous innovation built into their delivery cycles. However, there are still many application managed services masquerading as SaaS, which can slow innovation and complicate product upgrades. - AI:

Almost all CSP vendors now provide some form of AI within their platforms, but they do so in different ways. Prospective customers need to qualify which of the following approaches best suits their requirements:- Native embedded ML capability. This approach enables quick implementation, and imposes no additional costs, but is usually limited to a given set of use cases.

- Framework for ML. This approach offers a framework that enables the client to integrate with, and configure the output from, external ML engines. This method can be much more flexible, but imposes additional costs for implementation and ongoing usage.

- Hybrid of the above.

- Security and governance:

CSP vendors have long focused on providing fine-grained security control, but this has often been complex to manage and difficult for business users to understand. Increasingly, therefore, vendors are now using AI to automate security controls. Additionally, modern UIs can translate the underlying complexity of security management in terms relevant to business policy.

Die generellen Markteinschätzungen von Gartner:

„Market Overview

The dynamics of the CSP market continue to shift. This market has traditionally been dominated by long-standing vendors focused on operational content needs, but customers are now expecting more in terms of “consumerization” of the user experience and products that address new ways of performing business operations. The tension between digital workplace requirements (for ad hoc, collaboration-rich, day-to-day usage) and digital business requirements (for operational, process-rich usage) are resulting in:

- Continued expansion of SaaS-based vendors.

The reluctance of many organizations to put mission-critical content in a public cloud continues to decline. As it does so, vendors that have pure SaaS platforms and a well-developed information governance and security stance are gaining market share. - Modernization of long-standing platforms.

The shift in users’ expectations of, and new vendors now provide either new SaaS platforms or have rearchitected existing offerings to be more flexible and adaptable. - A broadening of scope by industry-specific vendors.

Vendors that previously focused on industry-specific use cases, particularly in the legal market, are expanding their offerings to address wider business needs. They are challenging other vendors in areas where information governance and security are priority requirements.

Three further key points relating to the CSP market in 2018:

- Both the CCP market and the CSP market grew in 2018. Revenue in the former increased to $3.8 billion, which raised its share of the total content services market from 33.7% in 2017 to 36.2% in 2018. The CSP market increased from $6.3 billion in 2017 to $6.8 billion in 2018.

- The ranking of the top-three CSP vendors — OpenText, Microsoft and IBM — was unchanged in 2018.

- The top-three vendors commanded 46.1% of the CSP market in 2018.„

Strategic Planning Assumptions

Gartner führt hier zwei Annahmen aus und schlägt die Brücke zu Content Collaboration Platforms (CCP):

- „By 2022, 20% of organizations will deploy content services evolved from a content collaboration platform (CCP) for digital business requirements, rather than a content services platform (CSP).

- By 2022, the current revenue growth rate for the CCP market will decrease from 34%, to match the CSP market’s growth rate of 8%.“

Neu hinzugekommen ist eine Übersicht zu den Quellen „Evidence“, die einen Einblick in die Arbeitsweise von Gartner erlaubt. Beim Quadranten muss man außerdem immer berücksichtigen, dass er nur eine Sicht auf die vorhandenen Daten bietet. Je nach Änderungen von Kriterien und Gewichten sehen die Positionierungen gänzlich anders aus. Diese spezialisierten Quadranten sind aber den Gartner-Kunden vorbehalten.

Magic Quadrant „Content Services Platforms“ (CSP) 2018

Zum Vergleich unsere Besprechung des Gartner Magic Quadrant Content Services 2018: http://bit.ly/GartnerCSMQ2018

Alle Quadranten von Gartner zum Thema ECM und ContentServices bei PROJECT CONSULT: hier im Update 2018 gibt es auf Folie 48 den Vergleich 2018 zu 2017 und hier im Update 2017 auf Seite 57 alle ECM-Qaudranten von Gartner 2007 – 2016.

Weitere Details zur Entwicklung des Marktes rund um ECM und Content Services bietet die Gartner peerinsights Zusammenstellung – allerdings nur für Gartner-Kunden: http://bit.ly/PeerInsightsCSP

OK

Wie immer sehr informativ. Danke für die kontinuierliche Veröffentlichung und Kommentierung von aktuellen Studien! Besonders interessant ist, dass die Investments in SER und die Übernahme von Docuware durch Ricoh positiv gesehen werden, da dadurch die beiden Anbieter aus Deutschland auch Zugang zu internationalen Märkten erhalten. Bei uns in Belgien spielen sie allerdings kaum eine Rolle.

Critical Capabilities for Content Services Platforms (CSP)

Ergänzend zum Magic Quadrant Content Services Platforms (CSP) 2019 hat Gartner nun am 30.10.2019 ergänzend die Critical Capabilities for Content Services Platforms Studie vorgelegt. Hier werden andere Blickwinkel auf die Informationen dargestellt. Die Kritik am Magic Quadrant richtete sich ja häufig dagegen, dass nicht ersichtlich war, auf Grund welcher Kriterien eine Einordnung geschehen ist. Gartner schreibt hierzu:

„What You Need to Know

Content services platforms (CSPs) are a vital part of any organization’s content services strategy. They are best aligned with use cases that cover the more formal aspects of how content is used in an organization. This is in contrast to content collaboration platforms (CCPs), which are often used in more informal, ad hoc collaboration. As such, CSPs typically provide advanced capabilities for document management, records management, workflow and content capture.

This report analyzes the capabilities of 18 of the major vendors in the market (there are 19 products included as one vendor — OpenText — has two products evaluated here). It does so by ranking a core set of 15 capabilities (described in the section titled Critical Capabilities Definition). The vendors are then further assessed by how well the capabilities support a set of five use cases, namely:

Content Application Composition

Document Management

Integrated Business Applications

Records Management

Team Workspace“

Die Kriterien und ihre Bewertungen sind am Ende der Studie ausführlich begründet. Es werden die gleichen Unternehmen wie im Magic Quadrant (siehe oben den Initial-Post) betrachtet: Alfresco, AODocs, Box, DocuWare, Everteam, Hyland, IBM, iManage, Laserfiche, M-Files, Micro Focus, Microsoft, NetDocuments, Newgen, Nuxeo, Objective, OpenText und SER.

Use-Case-Szenarien kombinieren 19 Basis-Technologien

Aus den Daten zu den Produkten der Anbieter wurden beispielhaft fünf Sichten als Szenarien generiert, die sehr unterschiedliche Rangfolgen für die Produkte und Anbieter zeigen. Dies zeigt auch, dass die Sicht mit MQ nur eine mögliche Darstellung ist, die sich im Tool von Gartner nach Bedarf selektieren, priorisieren und bewerten lässt.Die Kriterien der Bewertung und Gewichtung sind am Ende des Dokumentes erläutert. Die Studie kann bei beteiligten Anbietern – gegen Hinterlassen der Daten – z.B. bei M-Files kostenfrei heruntergeladen werden.

Einige Ausschnitte aus der Studie:

Analysis: Critical Capabilities Use-Case Graphics

(1) Content Composition Applications Use Case

Hier geht es eher schon in Richtung Content Services Applications und nicht um die Basis-Dienste. IBM mit P8, SER mit iECM und Hyland mit Onbase sind hier vorn. Bei den „klassischen“Anbietern bewegen sich die Bewertungen zwischen 4,54 und 3,85 – genaugenommen kein großer Abstand wie der Unterschied zu den folgenden Produkten zeigt.

(2) Document Management Use Case

Hier geht es um das klassische Dokumentenmanagement und nicht um die Sammelkategorie DMS, wie im Deutschen häufig falsch interpretiert. Hier sind IBM, Opentext extended ECM und SER vorn. Auch hier gibt nahezu die gleiche Schwelle wie in Abbildung 1 – von 4,61 bis 4,09 und dann ein Abfall.

(3) Integrated Business Applications Use Case

Auch hier wird schon in Richtung Content Services Applications geschaut – jenseits der Dienste in die Anwendungen. Es geht um die Integration und Anbindung von geschäftlichen Anwendungen. Ein Bewertungsabfall, der eher sanft ist.

(4) Records Management Use Case

Beim Records Management sind vorn wieder drei der „üblichen Verdächtigen“: OpenText, IBM und Hyland. Die US-Anbieter haben hier einen Heimvorteil, weil das Thema Records Management in den USA weitflächiger und stringenter ist. Die Unterschiede in den Bewertungen haben hier unterhalb von Microsoft einen steileren Abfall. Die gute Positionierung für Microsoft erklärt sich nur dann, wenn man sich die 2400-Seiten-Dokumentation für Records management in Sharepoint und O365 reingezogen hat.

(5) Team Workspace Use Case

Bei Team-Workspace im ECM/Content-Services-Umfeld hat sich längst Microsoft abgesetzt. Eigentlich sind wir hier auch eher im Umfeld des Gartner Magic Quadrant für Content Collaboration Platforms (CCP). Viele ECM-Anbieter setzen daher auch nicht mehr auf eigene Collaborations-Komponenten sondern binden Teams, Box oder ähnliche Produkte ein. Dementsprechend taucht auch Box oben in der Liste auf und müsste eigentlich noch einmal zur Position von IBM dazugerechnet werden.

Jeder der Anbieter mit seinem Hauptprodukt ist im Einzelnen im Text beschrieben und bewertet. Bitte lesen Sie den Text bevor Sie den Statistiken oben glauben.

Für den schnellen Zugriff haben wir Ihnen noch einige der wichtigsten Ergebnisse der Studie zitiert:

„Key Findings

Almost all CSP vendors are now offering some form of SaaS/PaaS solution. However, there are significant differences between the offerings when it comes to commercial terms, release cycles, underlying architectures and supported feature sets.

Artificial intelligence, mostly in the form of machine learning, is becoming a more common feature for content classification and enhancing productivity. A number of implementation patterns are emerging, ranging from fully packaged products to integration frameworks that utilize commercial machine learning service.

This is a relatively mature market, and stand-out features and functions can be difficult to find. Usability and simple/agile configuration are often key differentiators for this market.

Recommendations

Application leaders responsible for content services technologies as part of a digital workplace application strategy should:

Ask for details on parity between on-premises and cloud feature sets including the cadence of new releases and access to product upgrades. This is particularly important in private cloud instances where commercial terms can be more like an application managed service than SaaS.

Request details of the vendor’s AI architecture to ensure it matches the organization’s strategy for AI implementation. Deployment models for AI can vary from embedded native engines to a framework that requires additional commercial and technical input.

Include qualitative assessment techniques alongside feature questionnaires in RFP activities. At the most basic, this should be in the form of focused demonstrations that clearly articulate how these look for certain business scenarios and how such a scenario was configured.

Strategic Planning Assumptions

By 2022, 20% of organizations will deploy content services evolved from a CCP for digital business requirements rather than a CSP.

By 2022, the current revenue growth rate for the CCP market will decrease from 34% to match the CSP market growth rate of 8%.“

Quelle: Gartner, 30. Oktober 2019